Insight Focus

- The No.11 raw sugar futures strengthened over the past week.

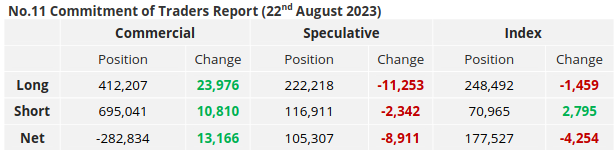

- Sugar producers and consumers have increased their hedging.

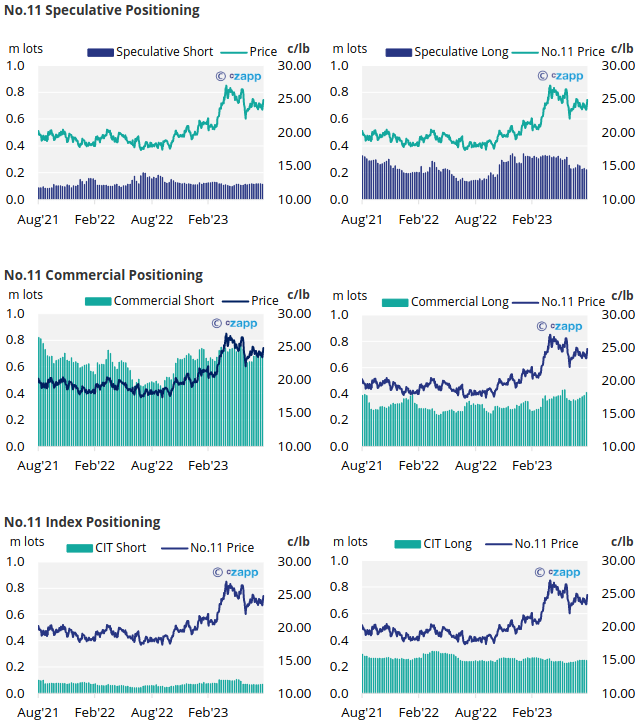

- The net speculative position has fallen slightly since last week’s update.

New York No.11 Raw Sugar Futures

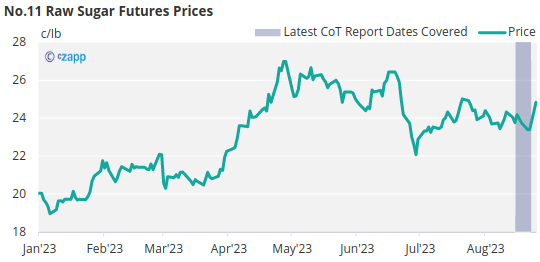

The No.11 raw sugar futures market rallied over the past week, with prices rising from 23.4c/Ib at the start of the week to 25.6c/Ib at the close of yesterday’s trading session.

For the second week in a row, both producers and consumers advanced their hedging. Raw sugar consumers added 23.9k lots of new long positions, mainly when prices were around 23c earlier in the week. Meanwhile, producers introduced around 10.8k lots of commercial short positions, likely as prices began to rally later in the week.

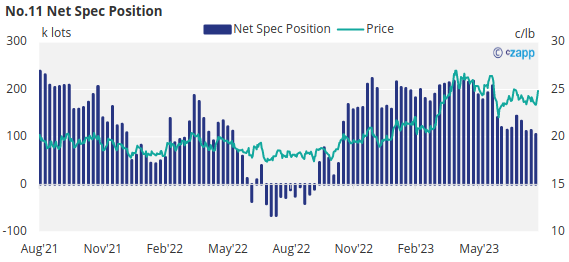

Looking over to the speculators, they have closed out 11.3k lots of long positions as well as 2.3k lots of short positions, reducing the overall net spec position to 105k lots.

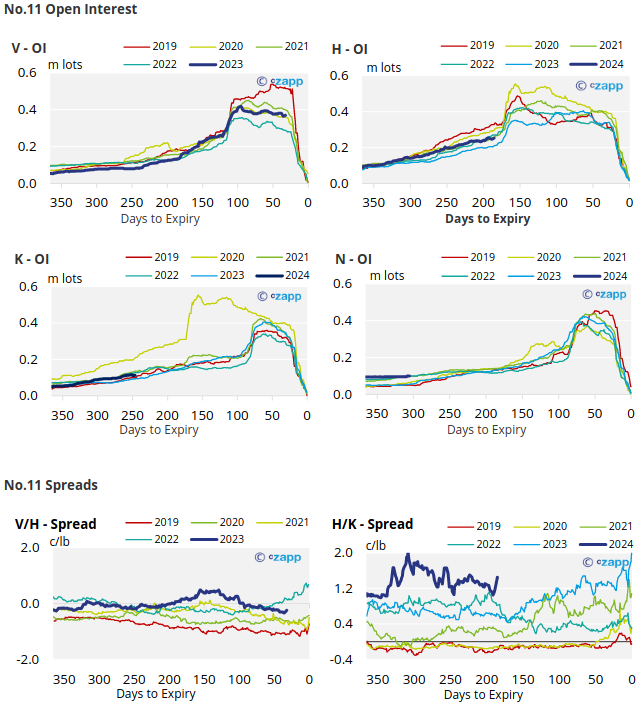

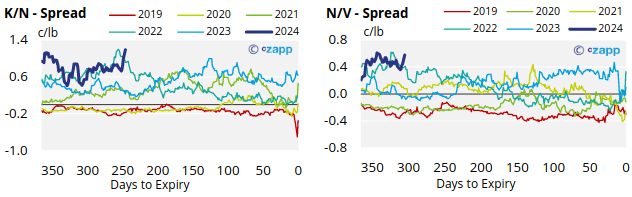

With contracts strengthening across the board, the No.11 curve remans inverted in 2024.

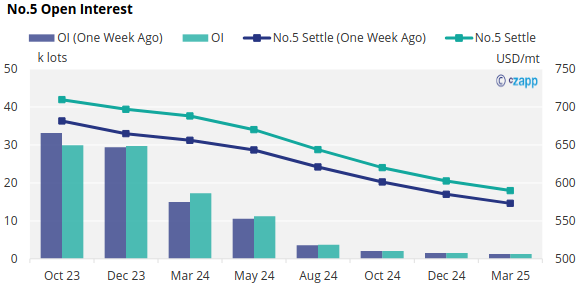

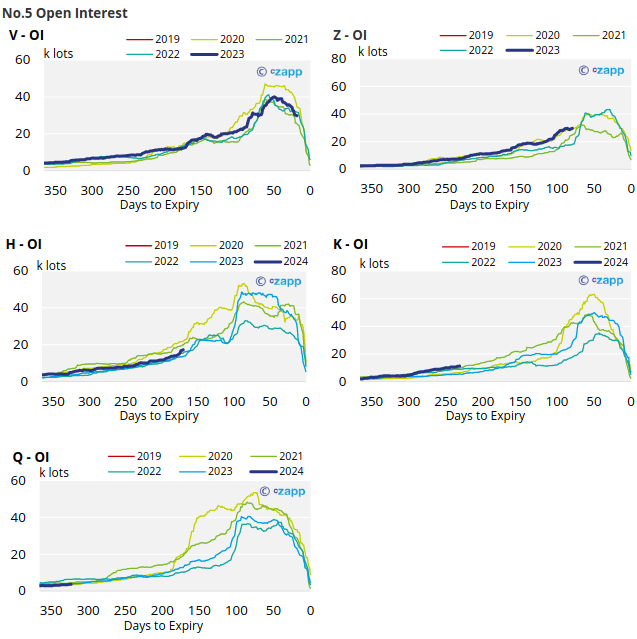

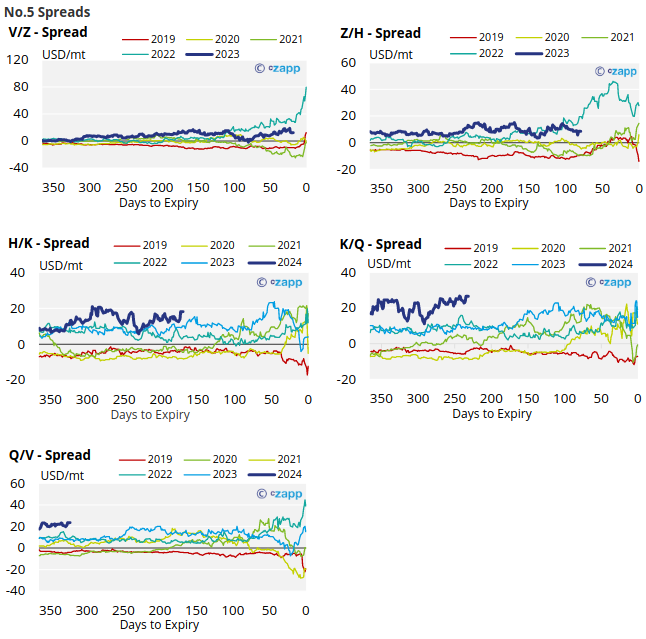

London No.5 Refined Sugar Futures

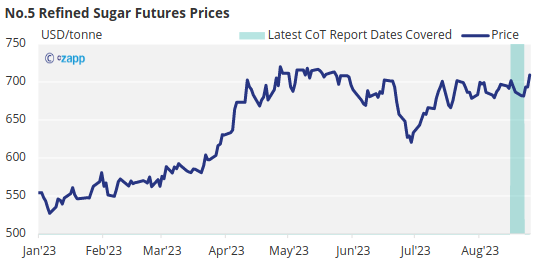

Following a similar trajectory to the No.11, the No.5 refined sugar futures has also strengthened, rising from 681USD/mt at the start of the week before closing yesterday at 709USD/mt.

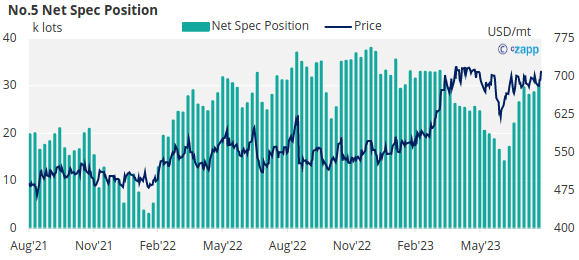

Speculators increased the net spec position by 1.6k lots last week, bringing the total net spec position to 30.2k lots.

With contracts strengthening slightly across the board, the No.5 forward curve remains inverted through to March 2025.

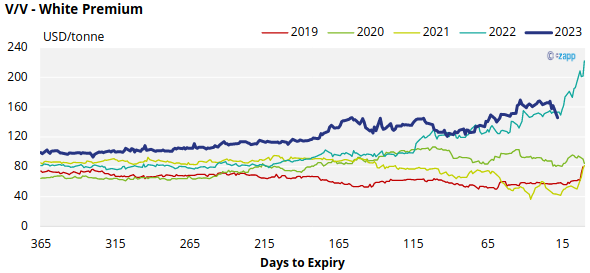

White Premium (Arbitrage)

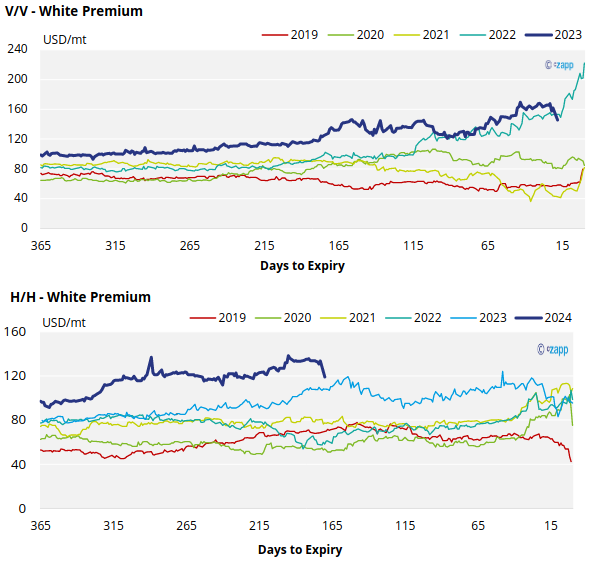

The V/V sugar white premium has fallen in the last week, and it now stands at 145USD/mt.

We think many re-export refiners require at least 85-100USD/tonne over the No.11 to operate profitably, this means the spot white premium offers comfortably enough for these refiners to be maximising their throughput.

At this level we could see higher-cost or discretionary refiners begin to consider re-exporting too, rather than just serving their domestic markets.

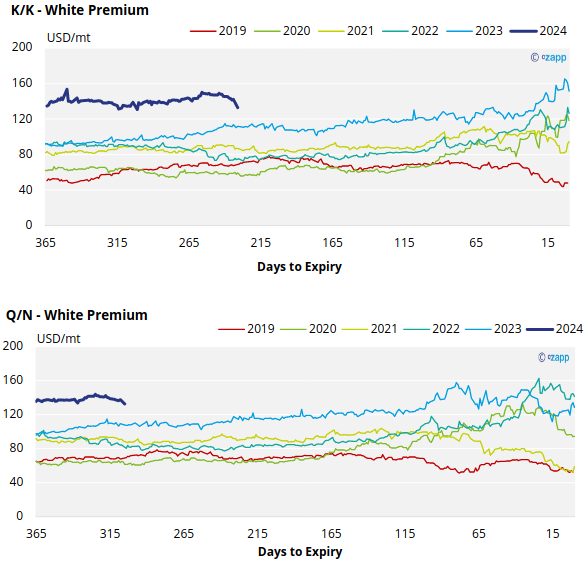

Whilst not quite as strong, the proceeding H/H, K/K, and Q/N white premium’s also comfortably offer enough margin over the No.11 for re-export refiners to be incentivised.

For a more detailed view of the sugar futures and market data, please refer to the appendix below.

No.11 (Raw Sugar) Appendix

No.5 (White Sugar) Appendix

White Premium Appendix