Insight Focus

- No.11 raw sugar prices have strengthened over the past week.

- As such, producers of raw sugar have increased their hedges.

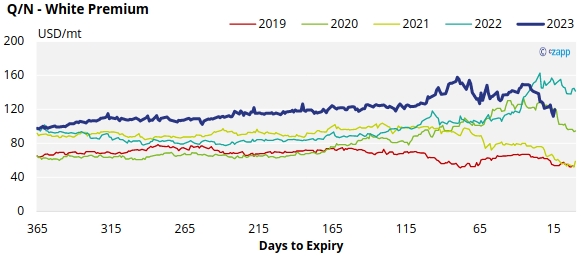

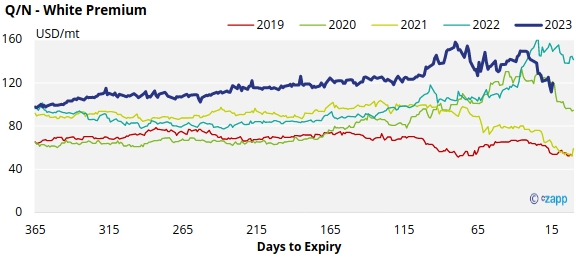

- Q/N white sugar premium has fallen in the last week, now standing at 119USD/mt.

New York No.11 Raw Sugar Futures

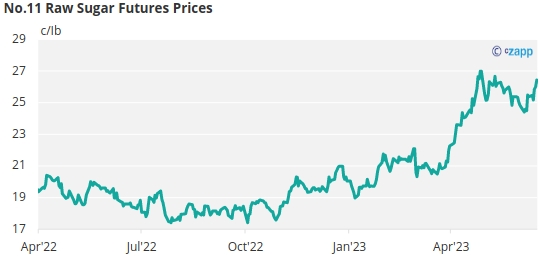

The No.11 sugar futures strengthened over the past week, closing at 26.4c/Ib by Friday.

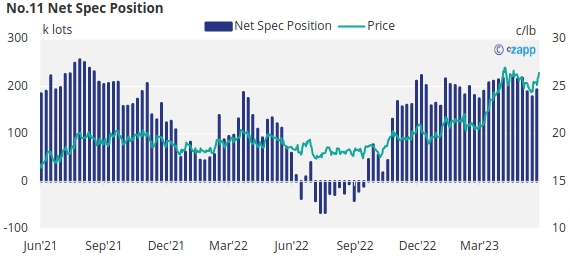

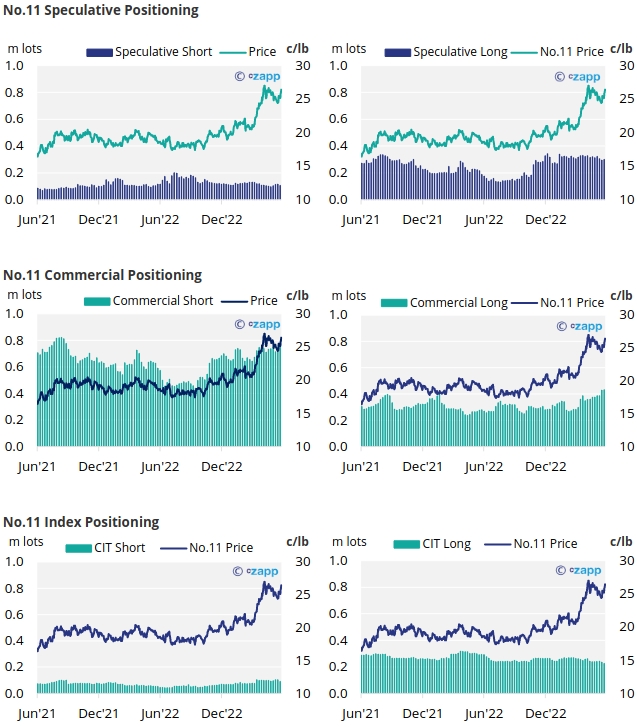

With prices reaching 26c/Ib, this provided a good opportunity for producers to sell. As a result, by June 13th (the most recent CFTC report), raw sugar producers had increased their hedges by 19.6k lots. There was also some consumer buying (2.5k lots), most likely hand-to-mouth before the Jul’23 expiry.

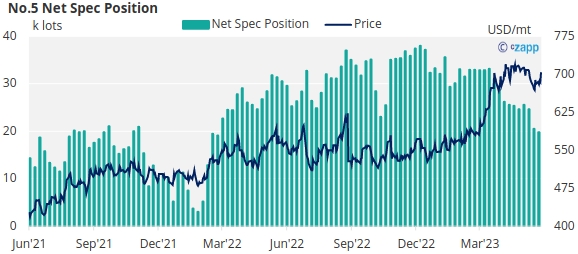

Over the same time frame, raw sugar speculators opened approximately 2.5k lots of new long positions and cut fewer than 9.2k lots of short positions. As such, the net spec position has extended by around 14.7k lots to 193k lots long.

The No.11 forward curve has become increasingly backwardated over the last week, particularly in the nearby contracts, this reflects current tightness in the raw sugar market.

London No.5 Refined Sugar Futures

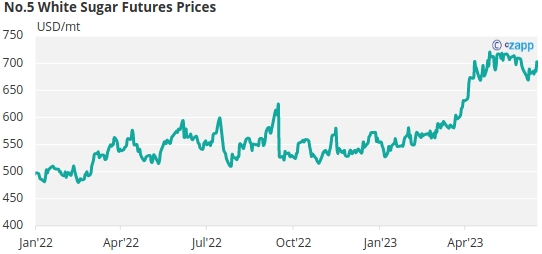

The No.5 refined sugar price has been trading sideways for the past week, before strengthening slightly to 702USD/mt by Friday’s close.

By the 13th of June (latest CoT data), refined sugar speculators reduced their long positions by 0.6k lots. The net spec position is now at 19.8k lots long, the lowest it has been since the start of 2022.

With contracts strengthening slightly across the board, the No.5 forward curve remains inverted through to December 2024.

White Premium (Arbitrage)

The Q/N sugar white premium has fallen over the past week reaching 119USD/mt by Friday.

Many re-exports refiners need around 110-120USD/mt above No.11 to produce refined sugar, so the current white premium is just enough to encourage this.

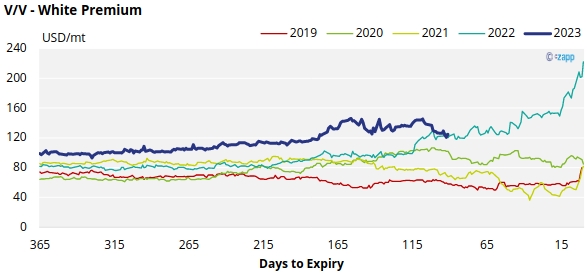

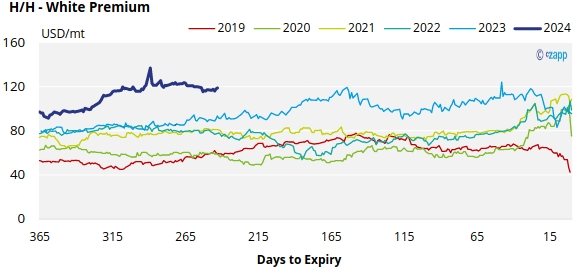

The refined sugar market is likely to be slightly undersupplied for the majority of 2023, and this is reflected in comparatively strong V/V and H/H white premiums, which has also weakened slightly over the past week and now approach 124.8USD/mt and 118.7USD/mt, respectively.

For a more detailed view of the sugar futures and market data, please refer to the appendix below.

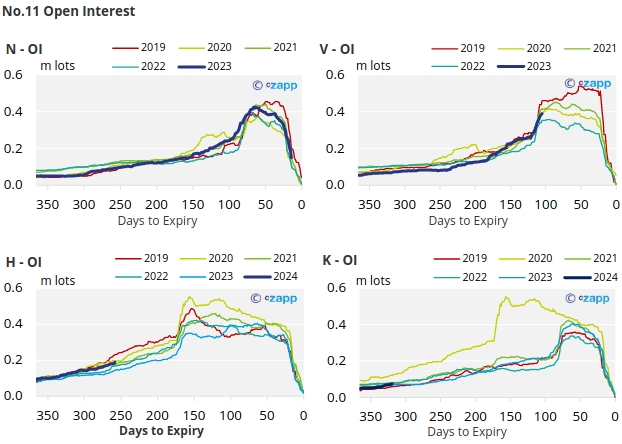

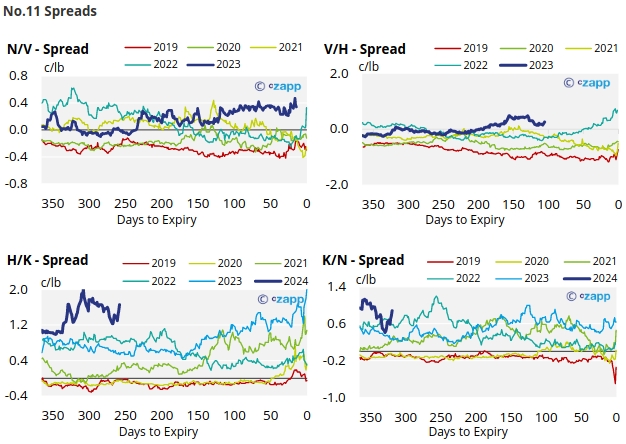

No.11 (Raw Sugar) Appendix

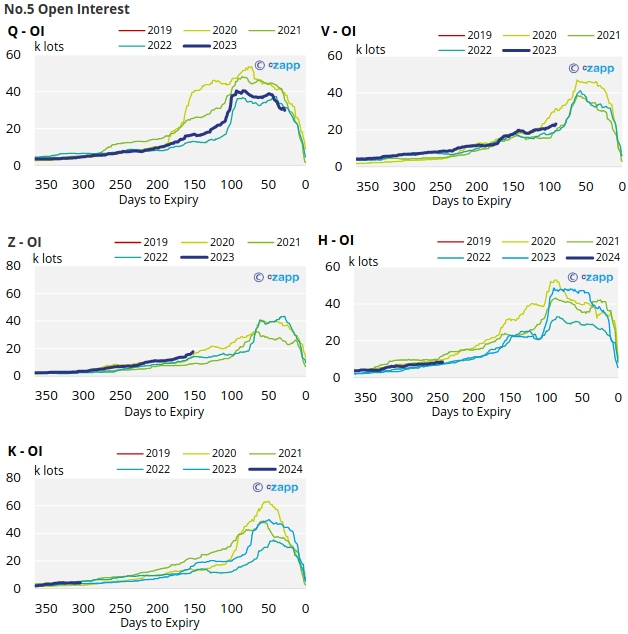

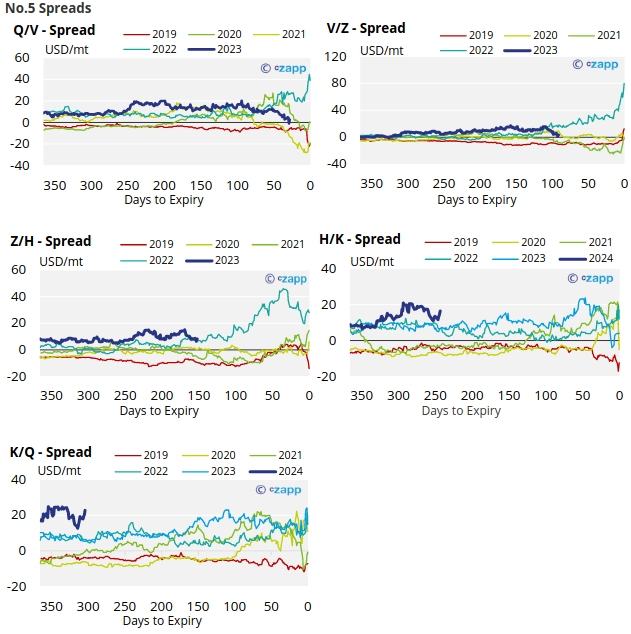

No.5 (White Sugar) Appendix

White Premium Appendix