Insight Focus

- The No.11 has weakened for a second week in a row.

- The net speculative position has also fallen.

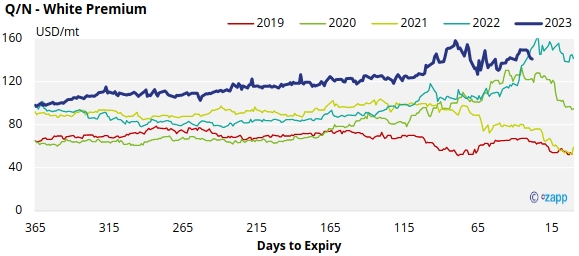

- Q/N sugar white premium has weakened slightly, standing at 141USD/mt.

New York No.11 Raw Sugar Futures

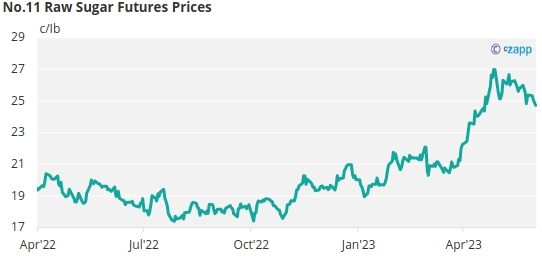

The No.11 sugar futures has weakened for a second week in a row, closing at 24.7c/Ib last Friday.

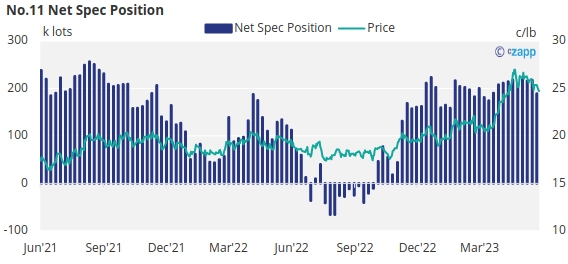

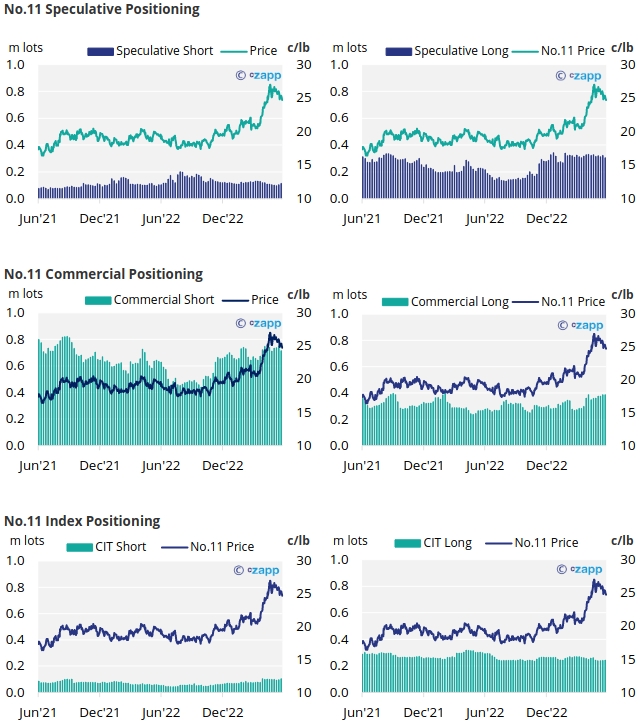

By the 30th of May (latest CoT CFTC report), the spec long position fell by 18.6k lots, less than 6% of the total number of long positions held last week. With an increase in the spec short position of 9.9k lots, the overall net spec position has fallen by 28.7k lots to 189k lots.

Looking over to the commercial side, raw sugar producers closed over 34k lots of short positions, while consumers closed only 0.4k lots.

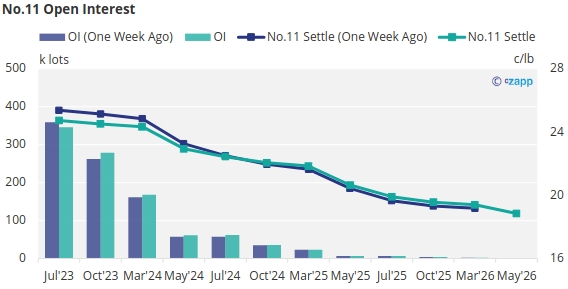

With prices down the board weakening over the last week, the No.11 forward curve remains backwardated.

London No.5 Refined Sugar Futures

Similar to the No.11, the No.5 sugar futures has also weakened over the past week, closing at 686USD/mt last Friday.

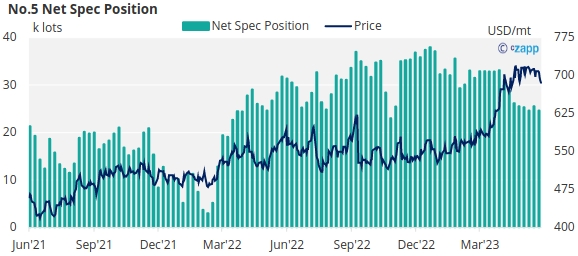

By the 30th of May with prices in decline, the refined sugar speculators reduced their net long position by around 0.9k lots.

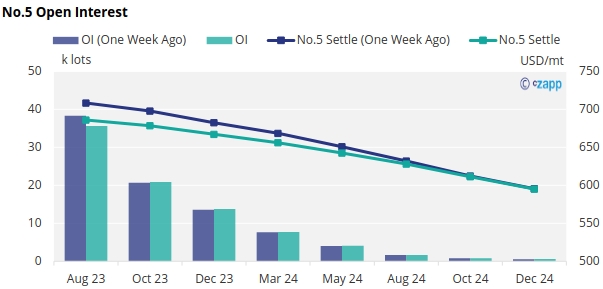

The No.5 forward curve remains backwardated as far ahead as Dec’24, suggesting a slowly easing market tightness over the next few years.

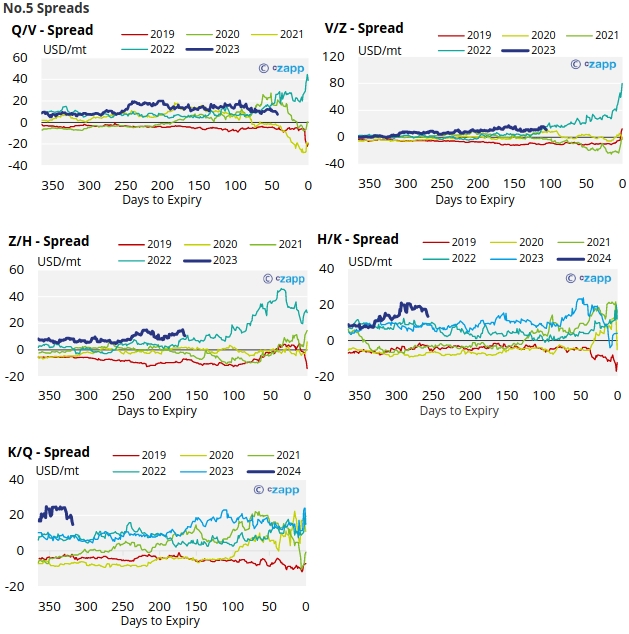

White Premium (Arbitrage)

The Q/N sugar white premium has strengthened slightly over the past week, now trading at 140.9USD/mt.

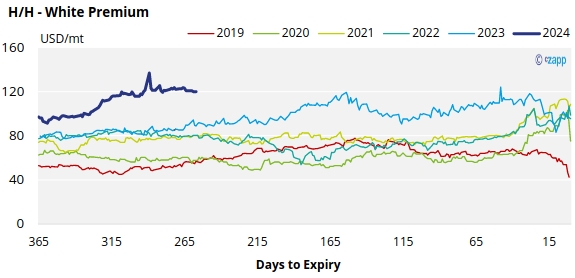

The refined sugar market is likely to be slightly undersupplied for the majority of 2023, and this is reflected in comparatively strong V/V and H/H white premiums, which have also been rising and now approach 138USD/mt and 120USD/mt, respectively.

With global energy prices falling, we believe re-exports refiners require around 120-135 USD/mt above the No.11 to produce refined sugar profitably.

For a more detailed view of the sugar futures and market data, please refer to the appendix below.

No.11 (Raw Sugar) Appendix

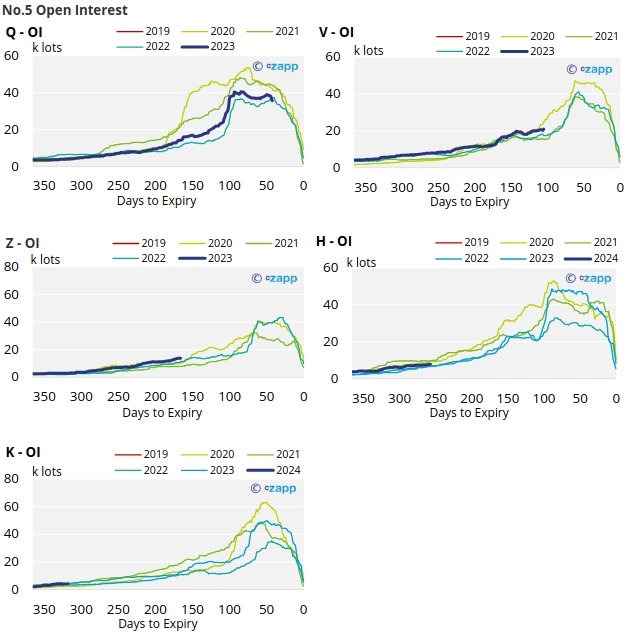

No.5 (White Sugar) Appendix

White Premium Appendix