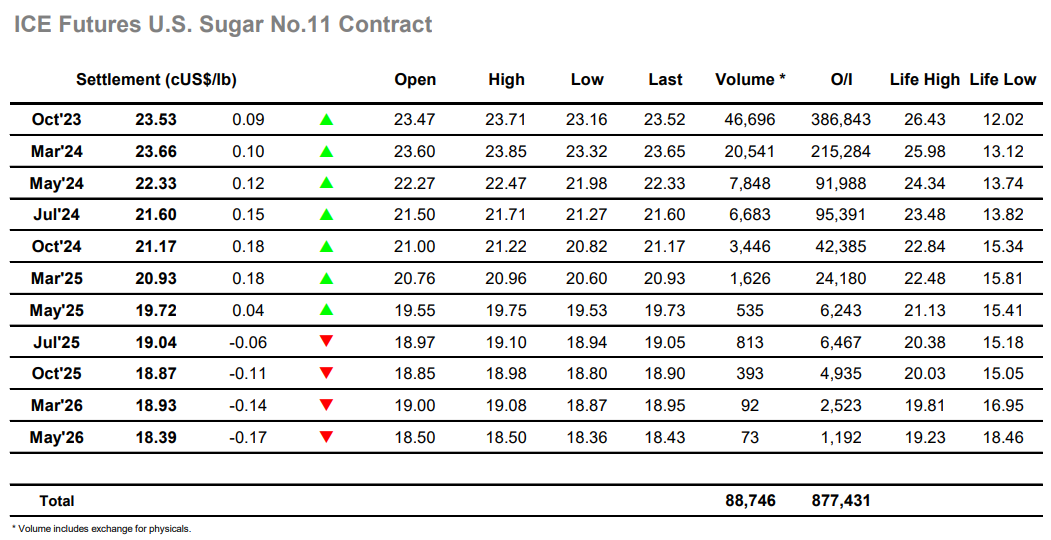

The day started with low expectations of anything other than a continuation of the recent range, and a lower start being followed by a steady rally to 23.60 did little to suggest this would not be the case. By late morning, the market was sitting quietly to the upper end of the range, with volumes having fallen to very low levels once more. The arrival of US specs brought no movement and suggests that they too are starting to find a sense of apathy towards the market, the only movement coming ahead of the latest UNICA announcement with a drop to a fresh daily low of 23.16 on expectation of further strong crop numbers. The announcement arrived showing that for the second half of June Brazil had produced cane at 43.003mmt / Sugar 2.695mmt / Mix 49.43% / ATR 133.04, and while the cane and mix were in line with expectation, it was the lower than anticipated ATR and resultant sugar total which drew a reaction. Oct’23 quickly rallied back to the 23.50 area with the sentiment then remaining positive through the rest of the afternoon with Oct’23 reaching 23.71. This still only left the market within the parameters of last week, and though prices remained firm heading into the final hour there was some day trader liquidation seen as the close loomed which left Oct’23 showing only a modest gain at 23.53. While today’s news will undoubtedly please the bulls it feels insufficient to boost the market back about 24c in isolation, and so a continuation of current conditions remains the most likely way forward.

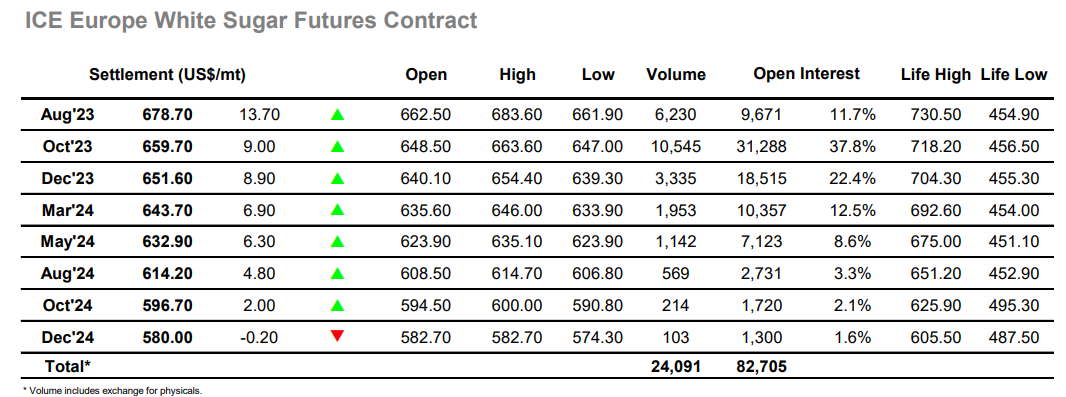

A weaker start to the session saw Oct’23 dip down to $647.00 initially, however in keeping with recent range bound trading there was soon some defensive buying emerging to send the market up again. With resting orders still minimal the market quickly gathered pace with an upside move to $659.10, fuelled by both spec interest on an outright basis as well as some solid trade buying of the nearby white premiums that saw Oct/Oct’23 widening out to $140.00. No.11 was meanwhile struggling to generate similar momentum and so once the inevitable profit taking kicked in prices retreated into the range, though they did not remain there for too long. Consistent efforts followed during the afternoon to try and move the market further north, and though they initially failed around the morning highs there was a persistence which eventually yielded success. Oct’23 marched all the way up to $663.60 while at the top of the board there was another strong pre-expiry showing for Aug’23 which reached $683.20 with the Aug/Oct’23 spread trading out towards $20. Aug/Oct’23 made an eventual high at $21.90 during the final hour before easing during the closing stages, with the flat price also falling back for nearby prompts against end of day position squaring. Oct’23 settled a few dollars shy of its high at $659.70, and while this still ensured a positive showing for the chart and a new recent high for the rally once feels that some assistance will be required from No.11 if the push higher is to continue and not simply represent a widening of last week’s range.