Insight Focus

Black Sea developments have impacted the wheat market. Continued volatility is driven by various weather issues across different continents.

There was a time when any negative development in either Russia or Ukraine would have significantly moved the market, but this is no longer the case. Lower production and weather challenges facing the new Black Sea crop in the coming months are noted but not met with panic. Missiles damaging ships in Black Sea ports now appear to be absorbed into daily news cycles.

Higher Russian export taxes, while still lower than previous rates, seem to have little impact as the Russian government attempts to establish increased price floors. Market participants observe these factors but no longer consider them remarkable.

Amid major conflicts and geopolitical discord, the market has developed an apathy towards these events, with business as usual continuing. Nonetheless, any market participant believing there cannot be a surprise price move ahead clings to this thought process at their peril.

Current Situation in the Black Sea

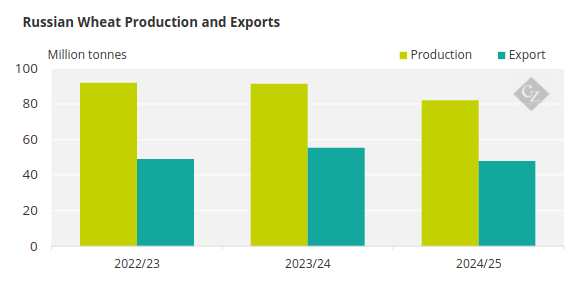

Russia’s 2024 harvest is estimated at around 82 million tonnes, down from 92 million tonnes in 2023. Consequently, exports are expected to drop by approximately 8 million tonnes from the 55 million tonnes shipped last year.

Source: USDA

Recent dry weather in the region has been interrupted by small amounts of rain, which must continue throughout the current drilling season to replenish soil moisture. Otherwise, wheat plants may struggle to germinate and establish themselves before harsh winter conditions, particularly early frosts.

In recent days, the Russian government has met with traders and begun to increase export taxes by 40%, while reportedly requesting a minimum FOB shipping price of USD 250/tonne.

The past couple of weeks have also seen a rise in Russian aggression toward Ukrainian Black Sea ports. Several foreign-registered bulk cargo vessels have been damaged, resulting in casualties and injuries.

Evolution of the Black Sea Situation

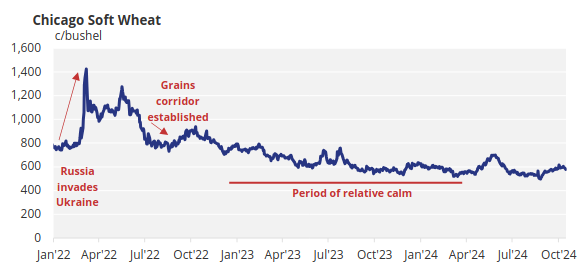

Before February 2022, when Russia invaded Ukraine, Russia and Ukraine were the largest and fourth-largest exporters, respectively, in the global wheat market, with the majority of shipments traveling through the Black Sea to North Africa and beyond. Russia’s invasion sparked an unprecedented rally in prices, raising fears for food security in the world’s poorest nations and importers.

The Black Sea grain agreement, brokered by Turkey and the UN in July 2022, facilitated the transport of particularly Ukrainian wheat and grains during a period of soaring prices.

Every disruption in this agreement heightened market anxiety as prices surged to all-time highs.

During 2023, the market calmed, and the long bearish trend continued into early 2024. Even Russia’s exit from the crucial Black Sea grain agreement in July 2023 resulted in only a short-term price rally.

As we approach the latter months of 2024, it appears that events in the Black Sea related to Russia’s war on Ukraine have little impact on the market, in stark contrast to the reactions observed in 2022.

Continued Volatility in the Market

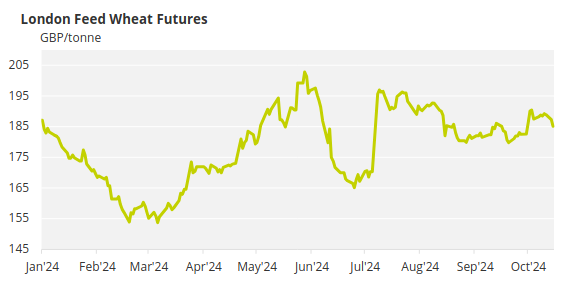

We do continue to see volatility in the market though, with prices falling from recent rally highs over the past few days. This decline primarily followed the latest USDA WASDE report released on Friday, which, although generally unexciting for wheat, added 500,000 tonnes to global end stocks for 2024/25.