Insight Focus

Corn prices diverged across exchanges last week. The strong US harvest contrasts with slow European progress. There is limited upside potential is anticipated for the market.

Corn prices moved in opposite directions on the Chicago and Euronext exchanges last week, while wheat traded mostly flat. EU production estimates for both corn and wheat were revised lower.

The primary concern remains the slow pace of harvesting in France, alongside quality issues for Black Sea corn. Price movements are expected to be largely influenced by the swift US harvest, where conditions are improving. We see limited upside potential for the market.

Our forecast for Chicago corn prices for the 2024/25 crop year (September-August) remains unchanged at an average of USD 3.90/bushel. Since September 1, the average price has been tracking slightly higher at USD 4.10/bushel.

Corn Prices Diverge Amid EU Forecasts

Corn prices diverged on the Chicago and Euronext exchanges last week, while wheat traded flat. EU production estimates for both corn and wheat were revised lower.

The week saw conflicting signals for corn: a strong US harvest pace contrasted with the October MARS report downgrading European corn yield.

The European Commission (EC) subsequently cut its corn production forecast, driven by lower output in Romania. Despite these downward adjustments, Chicago corn prices were stable, while European prices dropped sharply, influenced by the upcoming expiry of November futures.

The EC reduced its EU corn production forecast to 58 million tonnes, down from the previous 60.1 million tonne estimate, with the October MARS bulletin lowering the yield forecast to 6.66 tonnes/ha, below last year’s 7.48 tonnes/ha.

US corn harvest progress reached 81%, up from 68% last year and well ahead of the five-year average of 64%. Meanwhile, 76% of French corn was rated good to excellent, a one-point weekly increase but down from last year’s 83%.

Harvesting in France is lagging significantly, with 38% complete compared to 89% last year and an 81% five-year average. Ukraine’s harvest is 76% complete, with yields of 5.95 tonnes/ha, down from 7.07 tonnes/ha last year.

In South America, Brazil’s summer corn planting is 36.8% complete, while Argentina’s planting is at 34.5%, with 86% of the crop in good or excellent condition compared to 62% last year.

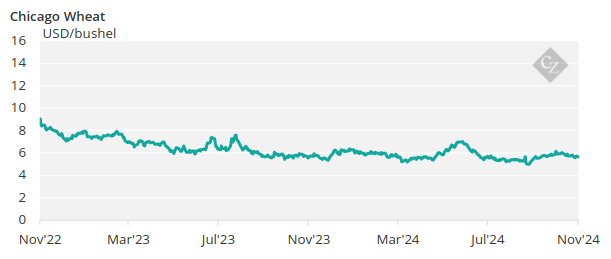

Wheat Market Holds Firm

In contrast to corn, wheat prices on both Chicago and Euronext remained steady, closing the week with minimal change. The EC adjusted its wheat production forecast to 114.6 million tonnes, down from the previous 116 million tonnes, primarily due to reduced output in France.

The first condition report for US wheat indicated a decline, with only 38% rated good to excellent, down from 47% last year. US winter wheat planting is 80% complete, close to the five-year average of 84%. In Ukraine, planting has reached 94% completion, while in France, it lags at 41%, well behind last year’s 60%.

The Russian wheat harvest is complete, yielding 87 million tonnes (gross) versus 97.3 million tonnes last year, with average yields of 2.97 tonnes/ha. The Russian Ministry of Agriculture’s clean-weight estimate is 83 million tonnes, down from 92.9 million tonnes last year.

Crop Outlook Influenced by Recent Rains

Brazil received expected rains last week, with additional rain forecasted across southern Brazil and Argentina’s agricultural zones. The US is also projected to have favourable rainfall across corn and wheat regions. North-Western Europe expects rain and milder temperatures, whereas Eastern Europe and the Black Sea region are likely to remain dry.

With Russia’s wheat production figures now official, the main area of uncertainty remains Germany, where delayed harvests and excess moisture may impact quality.

For corn, France’s slow harvest pace and quality concerns in the Black Sea region are notable, though Chicago’s quick harvest progress and improving conditions are likely to influence global price trends. We see limited upward pressure for the market at this time.