Yesterday’s bounce has reinvigorated some buying interest and though volumes were not huge during the early stages the market easily navigated its way up to 2.92 before pausing. These early gains were consolidated for a period with the stability then drawing some additional buying and pushing ahead to 22.00 where another pause took place. This seemed to have satisfied some day traders and profit taking followed to lock in the benefit from the movement, sending prices back into the range as noon arrived and allowing them to reset ahead of the US morning. A nudge back into the lower 21.90’s failed to gain any momentum during the early afternoon, unsettling any remaining longs and leading to a larger retreat ahead of the publication of UNICA data for the first half of November. The figures showed cane 16.46 mmt / Sugar 0.898 mmt / Mix 43.0% / ATR 133.09 kg/t / Ethanol 1.059 mlt, slightly below expectations of an already small number, but evidently not sufficiently low to inspire any additional buying despite placing stocks well below last years numbers as emphasised on social media ahead of the announcement. Whether this will be sufficient to get things moving higher at present remains to be seen with similar bullish posts having failed to have their desired impact last month, though many will be hoping that it can at least be a pre-cursor to the end of the present mundane situation. Having briefly printed into the red with a low at 21.57 the market managed to pull its way back up ahead of the close to post modest net gains at 21.69 and head into tomorrows Thanksgiving holiday with the wider picture unchanged.

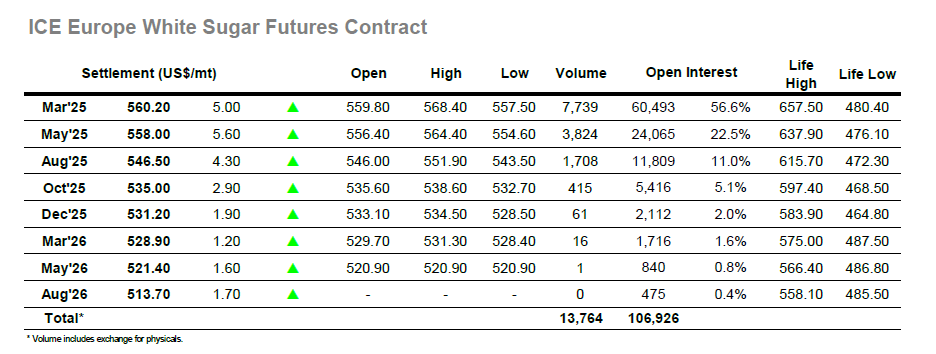

It was a strong start as March’25 gapped up on the intra-day charts, quickly pushing ahead to mark gains of more than $11 at $566.90 before pausing. This push gave the white premium a fresh shot in the arm with March/March’25 returning to $84, and with spreads also firmer there will have been more confidence in the recovery from longs than felt yesterday. This enabled the flat price to consolidate the upper end of the range, and while some selling filtered through later in the morning it still left a sizable gain in place. There would have been hops that the specs would look to push the market again during the afternoon to improve their book position, however that was not the case and instead the price eased back down to the opening lows amidst quieter conditions. Little occurred for a couple of hours until traders pushed the price down to $557.50 and almost filled the intra-day chart gap, and while there was a recovery back above $560.00 heading into the final hour it did not build any further. A mixed close saw March’25 settling at $560.20, the gains still leaving it firmly ensconced within the range, while March/May’25 ending lower at $2.20 shows that confidence remains fragile.