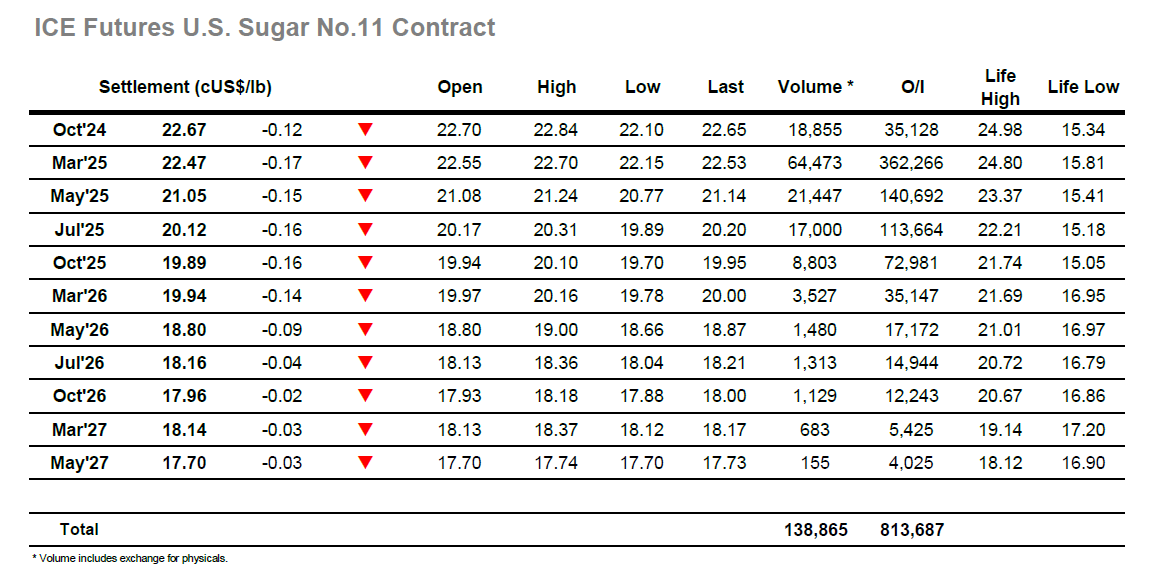

March’24 was trading either side of unchanged as the new week got underway, though the hangover of Fridays showing soon became apparent as the price descended to 20.24. The COT report on Friday showed a sizable rise in the spec long position to stand at 56,438 lots, though given the scale of the move during the reporting period some estimates around the market were for an even larger increase. Following a period of slow rangebound trading the market managed to claw back up to 22.70 around noon, however any effort to continue this move into the more active afternoon period soon petered out with the price returning to the 22.30’s by the time that US traders joined. Oct’24 was meanwhile enjoying its final trading session with some remarkably orderly trading, only light volumes now changing hands as the final position tweaks were made ahead of the tender and with Oct’24/March’25 showing no sign of significant movement away from Fridays 0.15-point valuation. Through the afternoon there was some expansion of the range to lows at 22.15, and these were revisited during the final half hour as it appeared that another sizable daily loss would be recorded. A late defensive push did ensure a close toward the centre of the daily range at 22.47 and significantly reduce the losses, while tomorrow will provide interesting viewing as we see how the market reacts to the delivery. Oct’24 expired at 22.67 with the Oct’24/March’25 spread valued at 0.20 points premium. A total of 33,506 lots (1,702,189t) will be tendered with full details to be published by the exchange tomorrow.

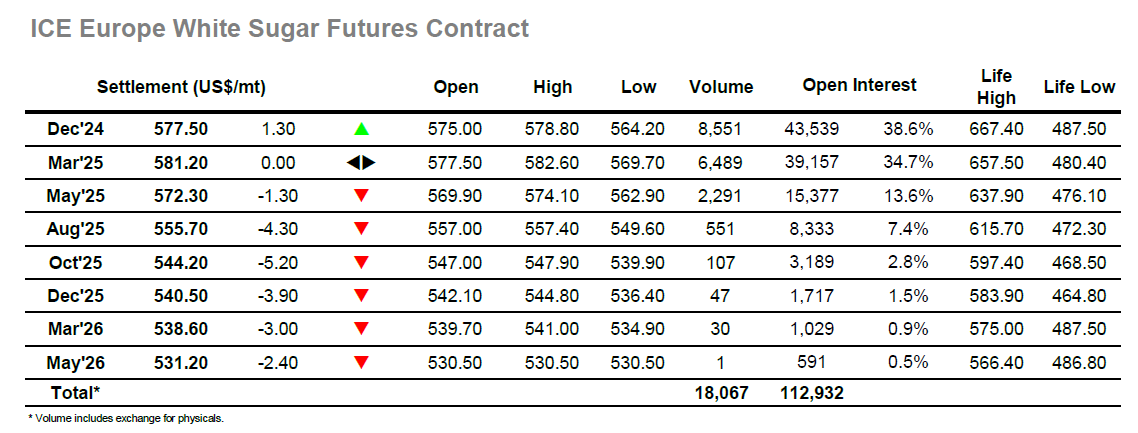

The whites are struggling to maintain higher levels without the drive of No.11, and this morning saw lower values through the first couple of hours with buying very limited above $570.00. There was a recovery to stand within touching distance of unchanged as we moved into the afternoon but that proved to be a flimsy recovery, and the lack of any sustained buying soon meant that prices were tracking lower once again. With the former gap now filled the market could have turned higher again but there was no enthusiasm for this with specs holding back and consumers still a long way above the levels at which they would want to conclude some sizable pricing. Having fallen back down into the range there was some long liquidation taking place which sent the price as low as $564.20, however once that had concluded the market was able to pull back upward on protective buying from longs keen to maintain the recent move and positive valuation that it provides. This enabled the March/March’25 white premium to work back up through the mid’$80’s and end the day around $86, with the flat price popping up into credit during the later stages. Dec’24 settlement at $577.50 will be viewed positively in the context of the day though plenty of work remains to be down if we are to work back above $600 and take another look at the recent highs.