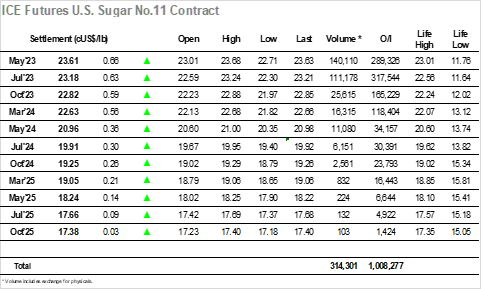

An opening peek to 23.05 did not yield any continuation of the buying and sop prices then set back with May´23 decline to 22.75 across a quiet first hour as some light profit taking took place. There was a little further erosion to 22.71 as the market looked to consolidate though by the later morning buyers had returned to continue their push higher with a fresh move to 23c. Pausing briefly beneath the morning high there was soon a continuation push which sent the price to 23.18, the movement coinciding with newswires reporting that there will be no additional Indian exports this season, despite that already being well accepted within the market. The move certainly seemed to be driven by specs, illustrated by the sharp liquidation drop to 22.93 once the progress had stagnated, though this turned out to be a mere blip in the progress and buying soon resumed once more. Sellers have been limited all the way up with many producers well priced and reluctant to add any further to potential margin stress, and with the trade and spec longs feeling that they have the upper hand in squeezing these shorts they looked to press home the advantage ahead of the long weekend. The price was driven ahead relentlessly to see May´23 trading at 23.60 ahead of the close, with a further push into the call seeing eventual highs recorded at 23.68. Settlement was reached at 23.61, and with another session to play out on Monday before we receive the latest COT data there may be more upside to come yet as the squeeze continues. The market is closed tomorrow while Monday sees a shortened session which commences at 7:30am NY time, with regular hours recommencing on Tuesday.

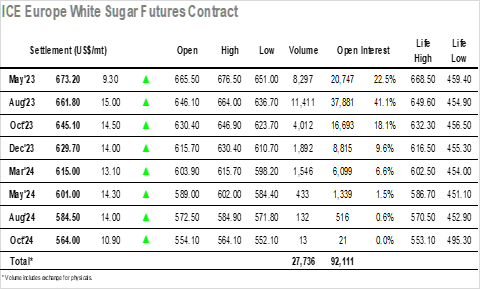

A moderately higher opening quickly gave way to some losses, a rare sight in the market recently where the colour red is hardly ever allowed to be seen. With buyers few and far between the Aug´23 contract dropped all the way to $636.70 before finding any support, though in the present environment a $10 correction doesn’t do significant harm to the picture. The rest of the morning saw prices steadily pulling back up through the range on light volumes, subtly moving back towards unchanged levels by early afternoon to be well poised to continue the current trend and end the shortened week on a positive note. Aug´23 was better set by this stage than the spot May´23 contract where spread selling was hitting the differential, and despite a brief foray to $21 early this morning the spike in values was largely forgotten as the price slipped back into the lower teens. The macro was providing no impetus; however, sugar continues to stand on it own recently and so as the afternoon progressed the latest in a long lost of rallies started to unfold. As ever it was the usual suspects driving the price higher, this time extending the price to $663.50 by the final hour, an incredible $26.80 above the morning lows. With such movement came swings in the white premium as Aug/Jul´23 swung between $144 and $153, though for the spread there was no such reprieve as the greater quantity of Aug´23 buying left May/Aug23 seeing a low at $10.70. A marginal new high was recorded at $664.00 heading into the close, leaving the market still incredibly well situated on the charts heading into the 4-day weekend, with settlements registered at $673.20 for May´23 and $661.80 in Aug´23.