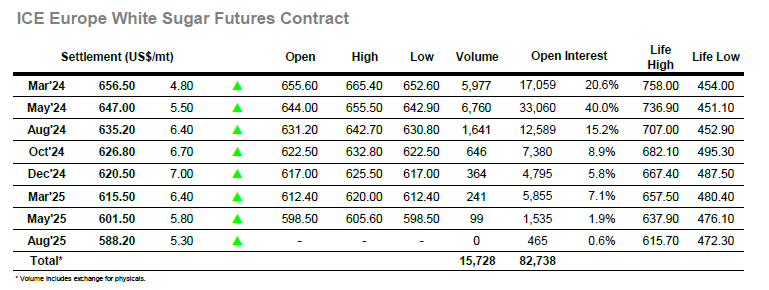

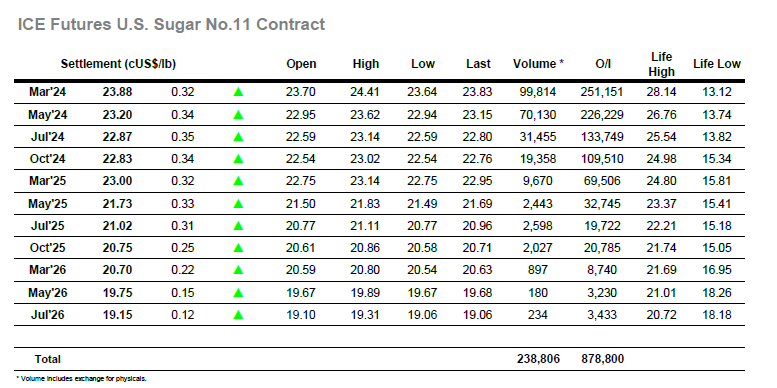

The day began with the market on the front foot with light opening buying sending March’24 up to 23.82, and with gains being maintained through the early period as price consolidated the 23.70’s. A mid-morning spike saw the price extend up to 23.98 however it was a brief foray only and soon the market returned to track along quietly within the range ahead of the Americas day. With volumes being dominated by the March/May’24 spread and Index roll the flat price remains open to wild fluctuation, and with the early afternoon finding a continued enthusiasm to extend the upside March’24 pushed through 24c. Successive waves of buying topped out first at 24.17 and then 24.41, though with some leeway in place for some of the long established on the push upward there was a more limited amount of profit taking being seen than is usual. The picture remained buoyant for a while with fresh efforts made to drive higher still later in the afternoon, though having fallen just shy of 24.41 the market finally saw some day trader liquidation. The release into limited buying saw a rapid drop to 23.80, and though some supportive buying then arrived for the call a settlement at 23.88 leaves the market still confined to the current range and likely to continue pivoting either side of 24c for the near term.  Recent days have seen the market continue to chop around wildly within the current broad range, and there was no sign of this volatility ending as initial activities saw the May’24 contract rise by around $5. Though these gains were not maintained the market was soon picked back up and with market depth remaining incredibly thin the price accelerated ahead to $651.30 before returning to the range against long liquidation, a familiar situation while the trade and larger funds stand aside. Early in the afternoon the market once again began to track higher against spec and algo driven activity, though as the price tracked higher it became apparent that the whites did not have the same drive as No.11. This was evidenced by the March/March’24 white premium which lost $6 across the afternoon to be trading at $128.00, despite the flat price seeing new weekly highs at $665.40 for March’24 and $655.50 for May’24. These highs were well supported through the later afternoon however there was a final twist during the last hour. Long liquidation sent May’24 tumbling back down to $644.90, a mere $2 above the early lows, and with settlement at $647.00 we remain firmly ensconced within the range for another day.

Recent days have seen the market continue to chop around wildly within the current broad range, and there was no sign of this volatility ending as initial activities saw the May’24 contract rise by around $5. Though these gains were not maintained the market was soon picked back up and with market depth remaining incredibly thin the price accelerated ahead to $651.30 before returning to the range against long liquidation, a familiar situation while the trade and larger funds stand aside. Early in the afternoon the market once again began to track higher against spec and algo driven activity, though as the price tracked higher it became apparent that the whites did not have the same drive as No.11. This was evidenced by the March/March’24 white premium which lost $6 across the afternoon to be trading at $128.00, despite the flat price seeing new weekly highs at $665.40 for March’24 and $655.50 for May’24. These highs were well supported through the later afternoon however there was a final twist during the last hour. Long liquidation sent May’24 tumbling back down to $644.90, a mere $2 above the early lows, and with settlement at $647.00 we remain firmly ensconced within the range for another day.