Insight Focus

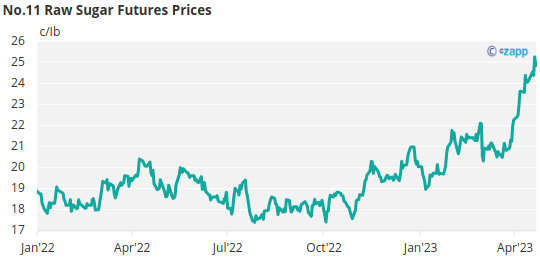

- No.11 raw sugar prices have strengthened over the last week, briefly reaching a 6-year high.

- Raw sugar producers and consumers have been closing out of positions in advance of the May’23 expiry.

- The refined sugar net spec position has weakened for the second week in a row.

New York No.11 Raw Sugar Futures

No.11 raw sugar futures hit a 6-year high of 25.6c/Ib last week, before closing at 24.8c/Ib by Friday.

With the May’23 contract close to expiry; attention is shifting to Jul’23, where prices closed just over 24c/Ib by close of trading on Friday.

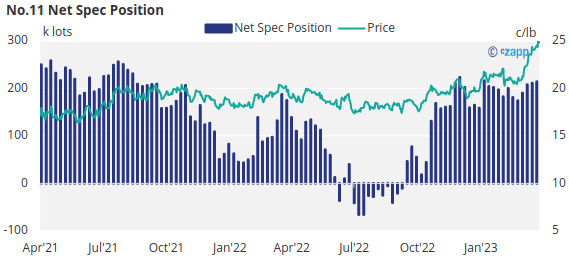

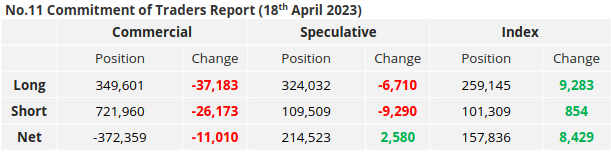

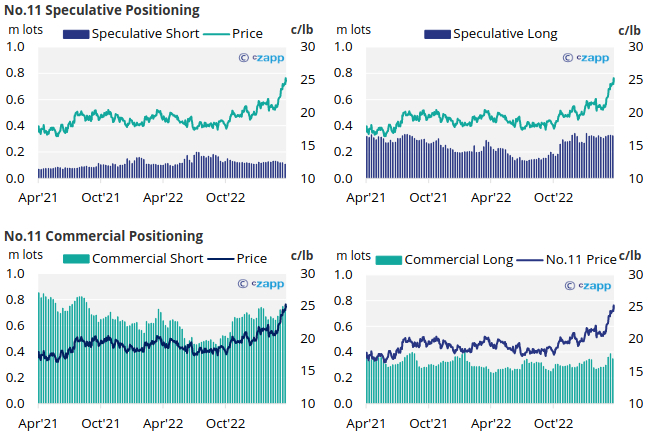

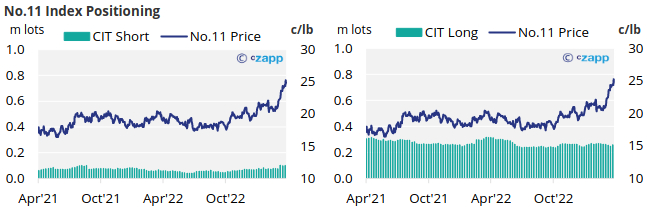

By the 18th of April (latest CoT CFTC), almost 7k lots of long positions have closed; with prices already at multi-year highs, speculators may be wary of the prospects for further price increases.

However, with over 9k lots of spec short positions closed compared to the previous week, the net spec position continued to extend slightly.

On the commercial side, both raw sugar producers and consumers have closed a significant number of positions, 26k lots and 37k lots respectively. This is likely just existing hedges being closed out as we move closer to the May’23 expiry.

The No.11 forward curve continues remains inverted until the end of 2025.

London No.5 Refined Sugar Futures

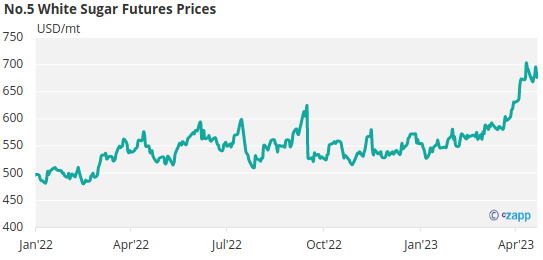

No.5 refined sugar futures strengthened to 697USD/tonne by Thursday last week before falling back toward 675USD/tonne on Friday.

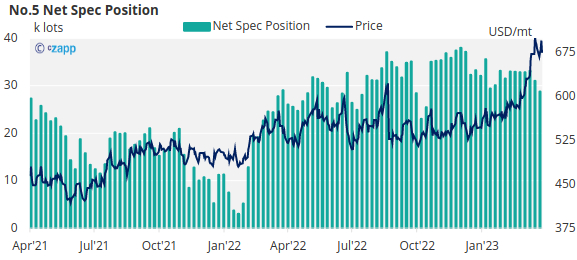

As of the latest CoT report from the 18th of April, the refined sugar net spec position weakened slightly, now standing at 28k lots long. This is still a large, long position for refined sugar speculators though does represent a reasonable drop for the second week in a row.

With contracts strengthening across the board, the No.5 forward curve remains inverted through to December 2024

White Premium (Arbitrage)

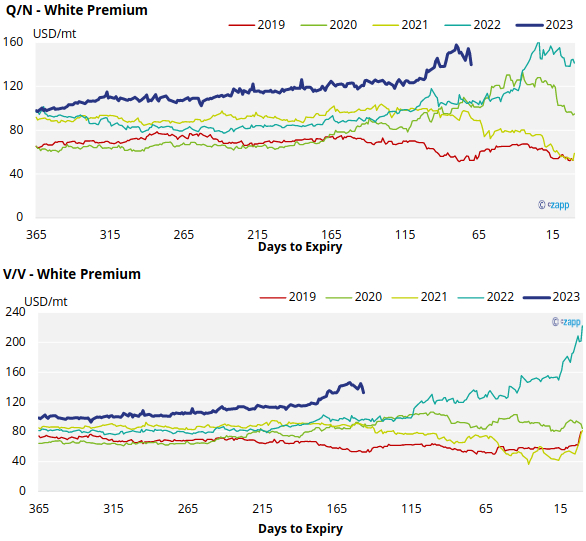

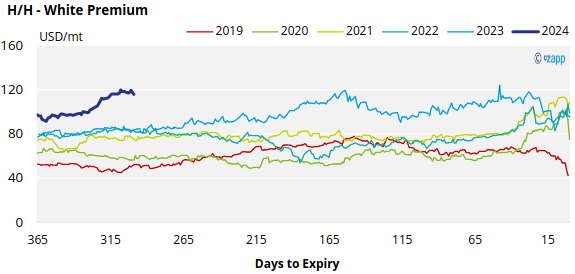

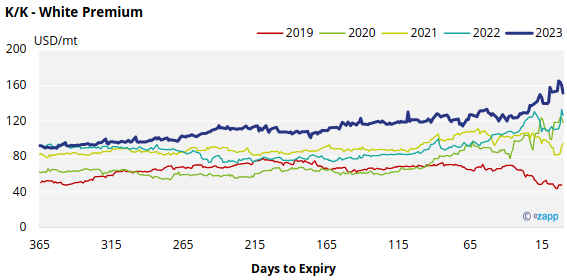

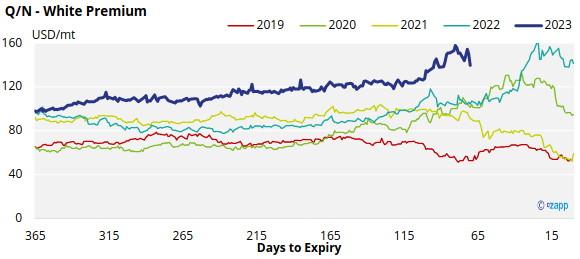

The Q/N sugar white premium has weakened slightly and is currently trading at 140USD/mt.

The refined sugar market is expected to be slightly undersupplied for the majority of 2023, as evidenced by comparatively strong V/V and H/H white premiums, which have also been rising and now approach 133USD/mt and 116UD/mt, respectively.

With global energy prices falling, we believe re-exports refiners require around 125-140 USD/mt above the No.11 to produce refined sugar profitably.

For a more detailed view of the sugar futures and market data, please refer to the appendix below.

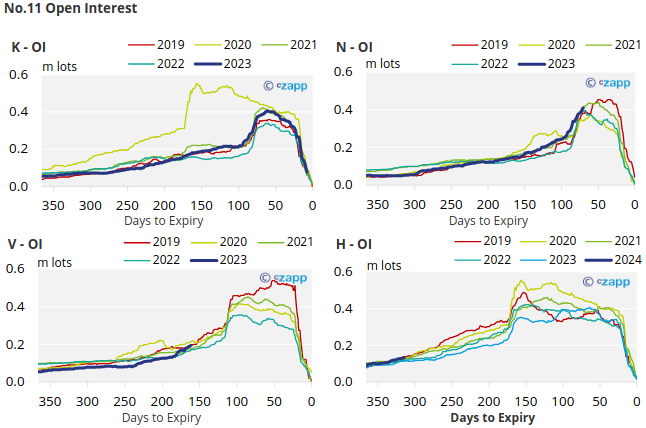

No.11 (Raw Sugar) Appendix

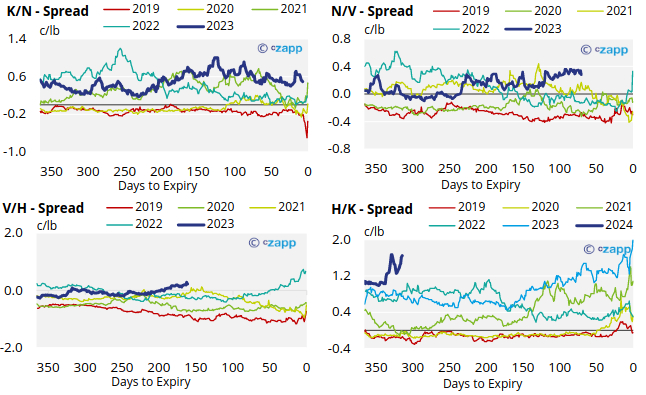

No.11 Spreads

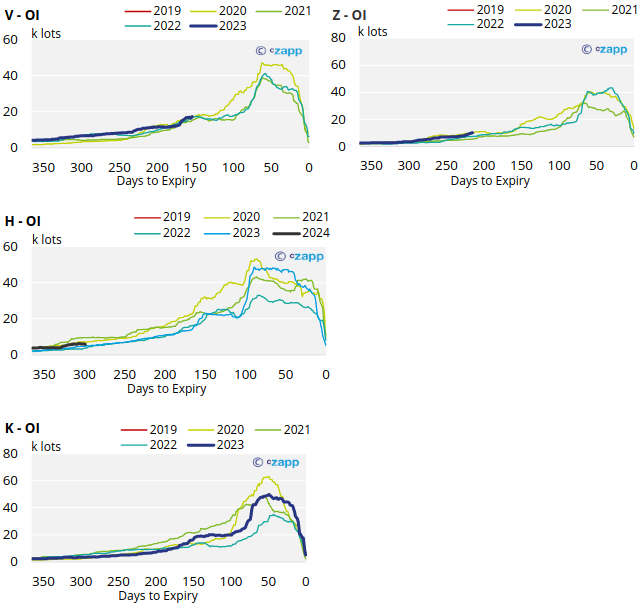

No.5 (White Sugar) Appendix

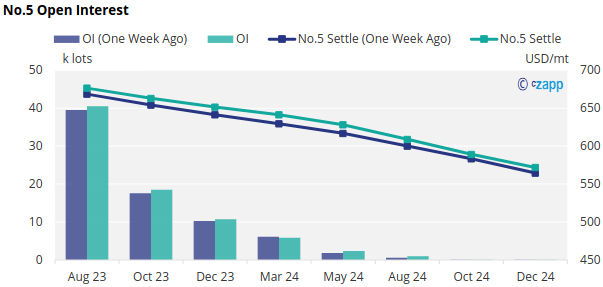

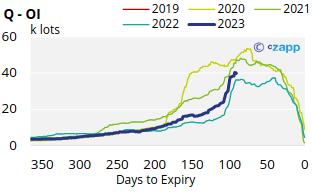

No.5 Open Interest

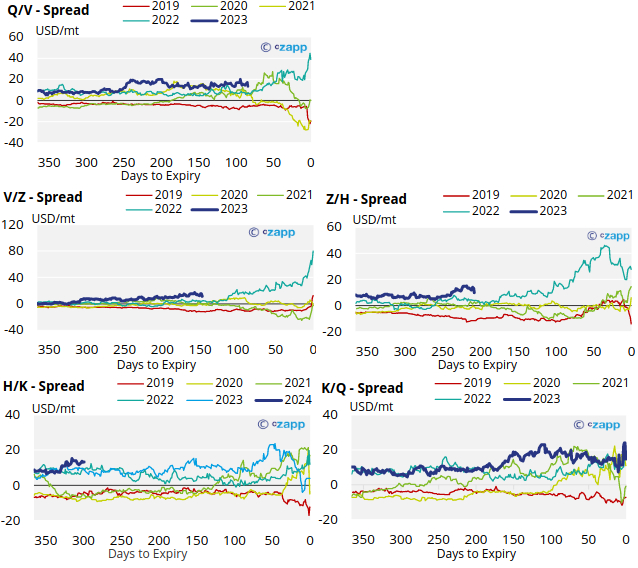

No.5 Spreads

White Premium Appendix