Insight Focus

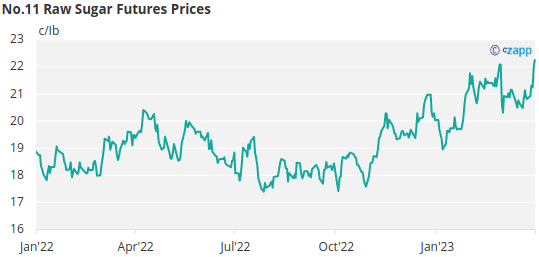

- No.11 raw sugar futures closed last week at 22.3c/Ib.

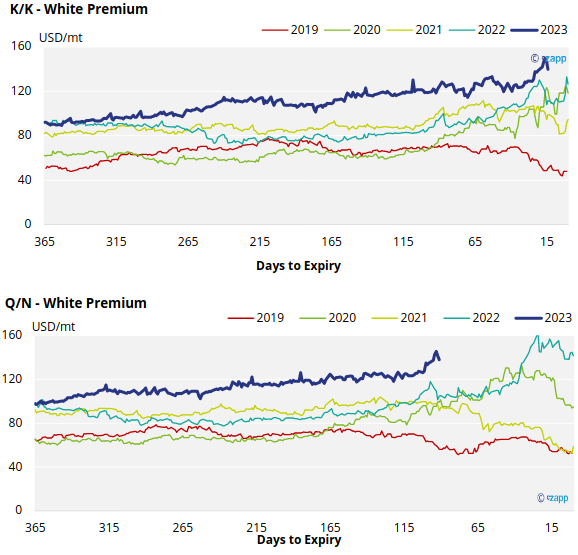

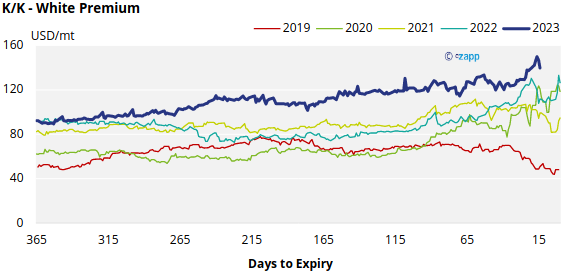

- K/K sugar white premiums have strengthened, standing at 139USD/mt.

- We continue to think that producers are well hedged.

New York No.11 Raw Sugar Futures

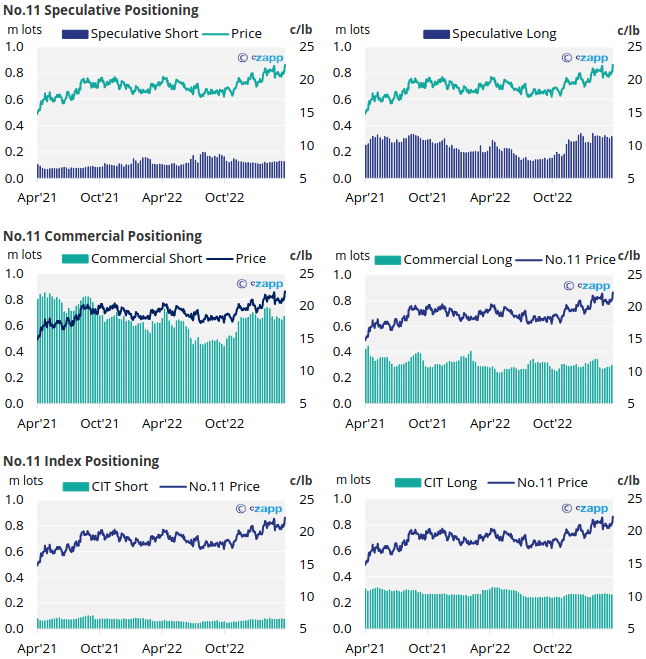

The No.11 raw sugar futures strengthened over the past week, closing at 22.3c/Ib last Friday.

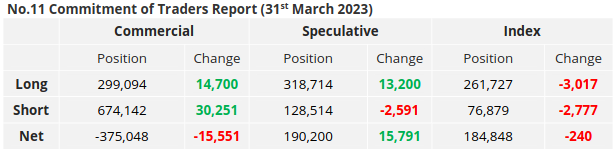

With this rally underway by the 31st of March (latest CoT CFTC report), raw sugar producers have added almost 30k lots of new hedges.

Despite market strength, consumers have been able to add 15k lots of new hedges, this was possibly hand-to-mouth buying in advance of the May’23 expiry.

Raw sugar speculators, buying into upwards momentum, have opened around 13k lots of new long positions and closed around 2.5k positions, which had likely come under pressure as prices began to rise.

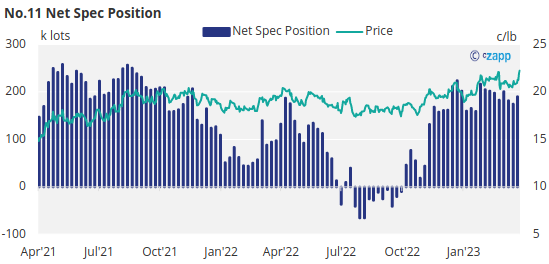

This means that the net spec position has extended for the first time in 3 weeks, reaching 190k lots long.

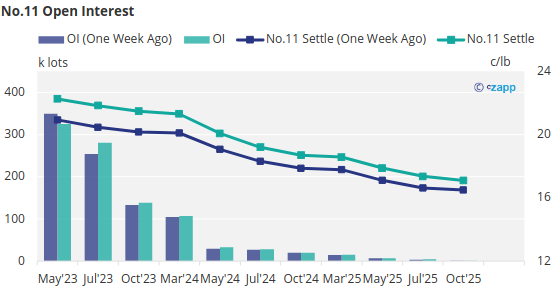

With contracts strengthening across the board, over the last week, the No.11 forward curve is now inverted.

London No.5 Refined Sugar Futures

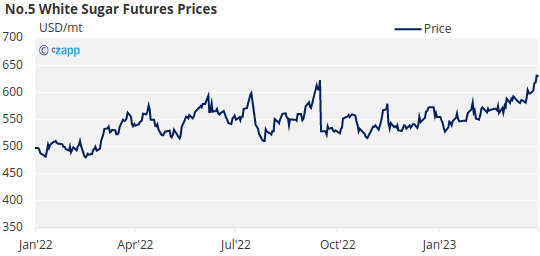

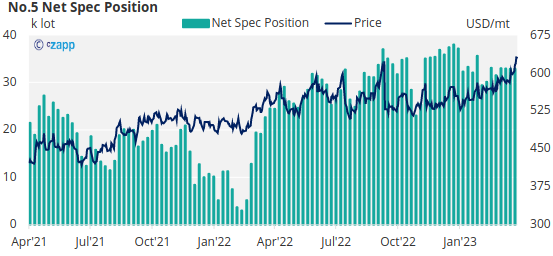

No.5 refined sugar futures have significantly strengthened towards the end of last week, closing at 630USD/mt on Friday.

Despite increase in the No.5 white sugar prices over the last week, the refined sugar net spec position has continued to remain stable, around 33k lots long.

In comparison to this time last year, when it was around 25k lots long, the net spec position is large and has been for the last 12 months.

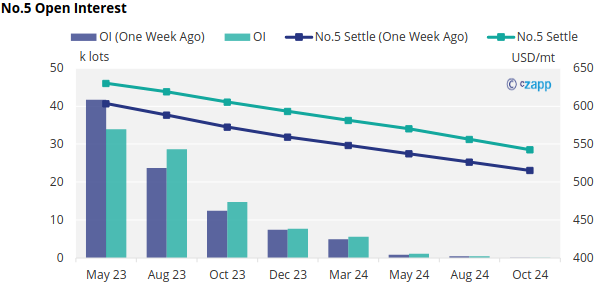

Currently, with contracts lifting across the board, the No.5 forward curve is inverted through to Oct 2024.

White Premium (Arbitrage)

The K/K sugar white premium increased slightly over the past week, closing at 139USD/mt on Friday.

With world energy prices falling, we think re-exports refiners need around 125-140USD/mt above the No.11 to profitably produce refined sugar.

For a more detailed view of the sugar futures and market data, please refer to the appendix below.

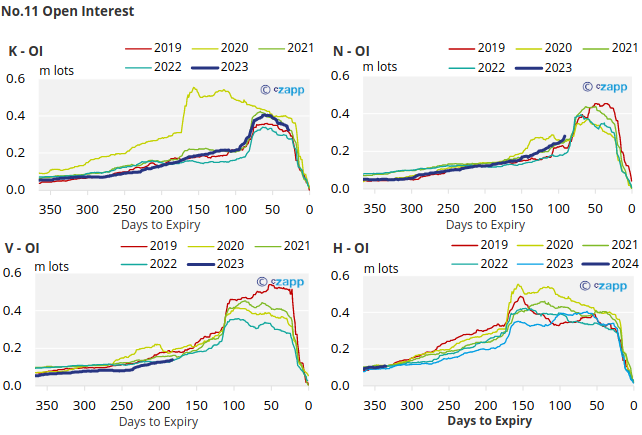

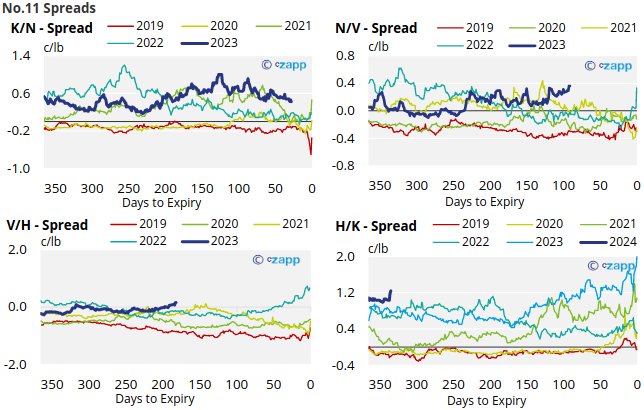

No.11 (Raw Sugar) Appendix

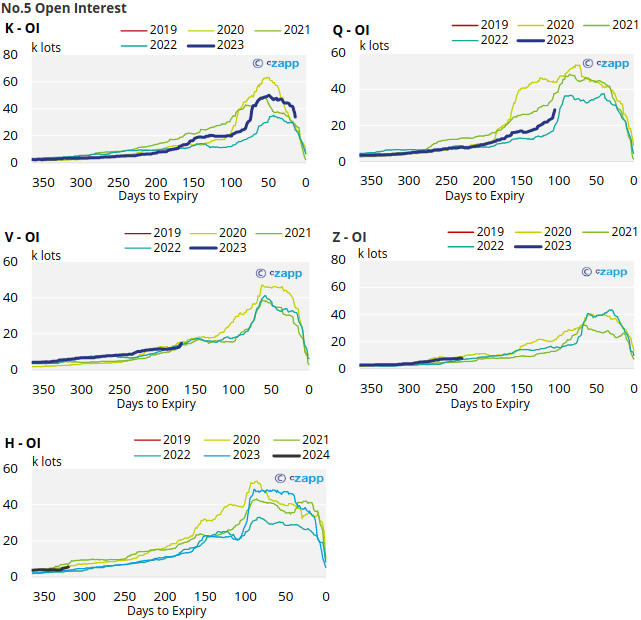

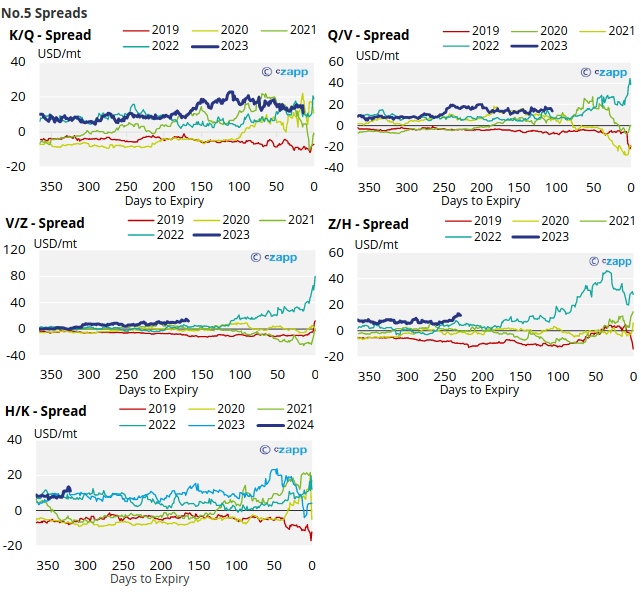

No.5 (White Sugar) Appendix

White Premium Appendix