Insight Focus

In 2025, new EU and US plastic waste laws are coming into force. They will boost demand for recycled PET and require supply chain adjustments. EU mandates will increase recycled content, while US states strengthen EPR laws. These changes will drive Design for Recycling adoption and rPET sourcing.

Plastic Waste Laws to Reshape Packaging in 2025

The issue of plastic waste will stay at the forefront of EU and US legislation in 2025, impacting on PET converters, packaging producers and the packaging supply chain.

The global plastic packaging industry is prepared for these changes, with the general consensus being that working together throughout the supply chain is what will guarantee the best possible outcomes for both the companies that rely on it and the circular economy.

From January 2025, legislative measures targeting packaging waste will bring significant changes to our old chum polyethylene terephthalate (PET). While some regulations are already in place, others are expected to take effect in 2025.

EU Mandates Boost Recycled PET Demand

All PET bottles in the EU are already required to contain at least 25% recycled plastic. This mandate is part of the EU Directive 2019/904, which has been established to reduce the environmental impact from plastic products.

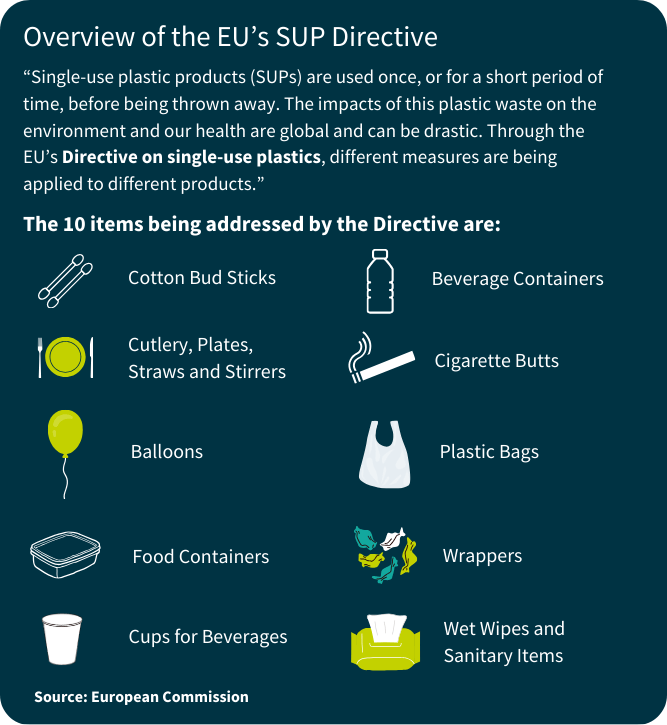

Widely known as the Single-Use Plastics Directive (SUP Directive), this key piece of legislation targets single use plastics and encourages collection and recycling of plastic products through clear targets.

PET converters and packaging producers are now required to adapt manufacturing processes to incorporate this mandated level of recycled material, which has already caused considerable impact in terms of availability and reliability of sourcing rPET. Many converters and PET packaging producers have subsequently needed to establish new sourcing strategies and integrated technological adjustments.

It’s likely the PET supply chain will be impacted in 2025 due to this increased demand, so any preparations to encourage the robustness or reliability of a converters rPET supply is a good plan. This demand for high quality rPET will most likely force the issues surrounding insufficient recycling infrastructure too.

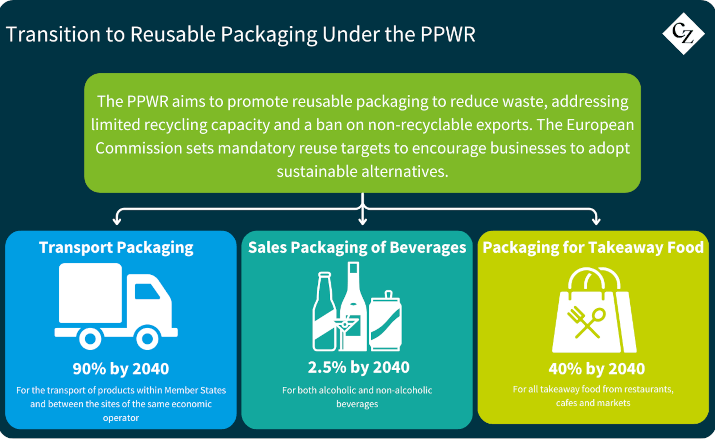

The widely reported EU Packaging and Packaging Waste Regulation (PPWR) implementation timeline means that the PPWR will replace the previous Directive 94/62/EC, expected by the end of 2025.

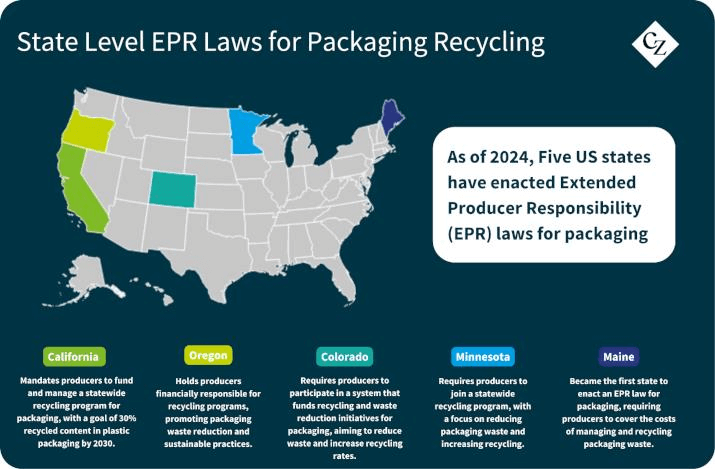

US States Set to Strengthen EPR Laws

This year, it is likely that US states like California, Maine, Colorado and Oregon will cement their commitment to the Extended Producer Responsibility (EPR) Laws, which require producers to fund recycling programs and meet specific recycled content volumes.

This will impact on PET converters and packaging producers with the increased financial responsibility for end-of-life management of their products, so expect greater promotion and adoption of Design for Recycling (DfR) principles as standard.

The legislative developments set for 2025 aim to promote sustainability within the plastic packaging industry, but they will require significant adjustments from PET converters and packaging producers across the supply chain to ensure compliance and maintain market competitiveness.

Those with a reliable supply of rPET and a deep understanding of DfR guidelines will likely have a head start.